There are some life lessons people learn the easy way. Others they learn with a deed. Some are learned through a breakup. And some come with a bank statement.

This is one of those.

Every day, smart people make major property decisions based on love, trust, and shared plans. They buy homes together, move money around, split bills, pay for repairs, and build a life. And because the relationship feels solid, they assume the legal part will work itself out later.

It often does not.

That is the problem with mixing real property and real feelings. One runs on hope. The other runs on paperwork.

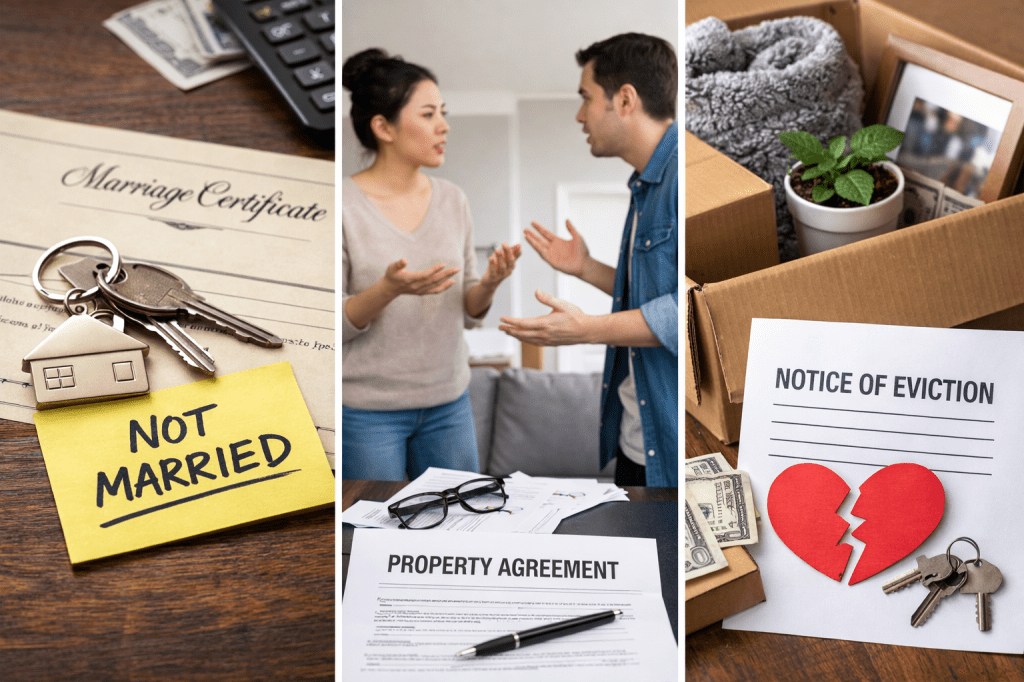

If you are buying a home with someone you are not married to, hear me clearly: love is not a property agreement.

The law does not run on vibes

People hate when lawyers say that, but it is true.

The law is not usually moved by what was understood “between us,” what somebody said in the kitchen, or what seemed fair during the good part of the relationship. The law looks at title, written agreements, records, payment trails, and conduct that can actually be proven.

So yes, you may have picked out the house together.

Yes, you may have both made sacrifices.

Yes, you may have both called it “our home.”

But when things go left, the legal question becomes much less romantic: whose name is on what, who paid what, and what was actually documented?

That is why people get blindsided.

Paying is not always the same as owning

This is the part that stings.

A person can help with the down payment, contribute to the mortgage, pay utilities, fund renovations, and carry the household in practical terms, and still not have the legal ownership interest they thought they had.

That does not mean there is never a claim. It does mean people routinely overestimate how much protection comes from contribution alone.

In plain English: just because you put money into a house does not automatically mean the house legally belongs to you too.

It sounds cynical, but really, it’s just caution.

Too many couples discuss paint colors before exit plans

I have said it before and I will say it again: many couples spend more time choosing countertops than deciding what happens if one person wants out.

That is backwards.

Before you buy property together, the grown-up conversation is not just:

- What neighborhood do we want?

- How much yard space do we need?

- Can we make the kitchen more open concept?

It is also:

- Whose name is going on title?

- Are we owning this equally?

- Who is paying what?

- If one person puts in more money, does that change the ownership split?

- If we break up, who keeps the house?

- Can one person buy the other out?

- If we sell, how is the money divided?

- What happens if one person dies?

It feels like you’re being negative, but really, you are being disciplined.

The most expensive phrase in these situations

You know what gets people in trouble?

“Don’t worry, we’ll figure it out.”

That phrase has cost people equity, leverage, peace, and years of litigation stress.

Because by the time “we’ll figure it out” becomes “you never said that” or “that was never the deal” or “you were just helping with bills,” the relationship has already changed. And once the relationship changes, people remember the past very differently.

That is why documentation matters when everyone is still smiling.

Family property makes this even messier

Now add family into it and the situation can get even more delicate.

Sometimes a person moves into a house owned by their partner or their partner’s family. Sometimes they pay for repairs, remodeling, taxes, or upkeep based on promises about the future. Sometimes they are told, in one form or another, “this will all be yours one day,” or “we are building this together.”

That may be emotionally meaningful. It is not the same thing as present legal protection.

Future inheritance plans, family assumptions, and verbal assurances are shaky ground to build a financial life on. If your name is not on title and your rights are not in writing, you need to understand the risk before you keep investing.

What wise women, wise men, and wise parents do

They get it in writing.

Not because they expect failure. Not because they are unromantic. Not because they do not trust the person they love.

They get it in writing because property is serious. Money is serious. Stability is serious. Children, housing, and long-term wealth are serious.

A written agreement can clarify:

- who is contributing what

- whether ownership is equal or unequal

- how monthly expenses are handled

- whether there is a buyout option

- how repairs and improvements are treated

- what happens if the relationship ends

- what happens if one person wants to sell before the other does

That kind of clarity is not cold. It is protective.

And if we are being honest, protection is part of love too.

If the relationship has already turned

Once things start shifting, people often make the situation worse by moving too fast emotionally and not fast enough legally.

They move out without a plan.

They stop paying without understanding the consequences.

They sign things to “keep the peace.”

They send long angry texts that later become exhibits.

They trust that fairness will win without ever gathering proof.

No. Gather the paper.

Get the deed. Get the purchase documents. Get the mortgage records. Get the receipts. Get the bank statements. Get the texts and emails. Build the timeline.

Because a property dispute is rarely improved by panic. It is usually improved by records.

This is bigger than a breakup

What people often miss is that these disputes are not only about romance ending. They are about wealth, leverage, housing, and long-term stability.

For many people, a home is the biggest asset they will ever touch. So when unmarried couples buy property casually, they are not just being casual with feelings. They are being casual with equity.

And equity has a way of becoming very important very quickly.

Final Thoughts

Let me say it plainly.

If you are unmarried and buying property with someone, do not confuse closeness with legal clarity. Do not confuse shared plans with secured rights. Do not confuse contribution with ownership. And please do not confuse “we good” with “we protected.”

A house can be a blessing. It can also become a battlefield when nobody handled the legal side with maturity on the front end.

Love may have brought you to the closing table.

But love is not what will sort it out if things fall apart.

Paper will.

***************

Disclaimer

This post is for general educational purposes only and is not legal advice about any specific situation.

Leave a comment